.

The content displayed on this page is intended for guidance purposes only. It is not exhaustive and is constantly being updated to reflect the latest changes. To stay up to date, we advise you to visit this page frequently.

Get your e-commerce business ready for the new VAT rules

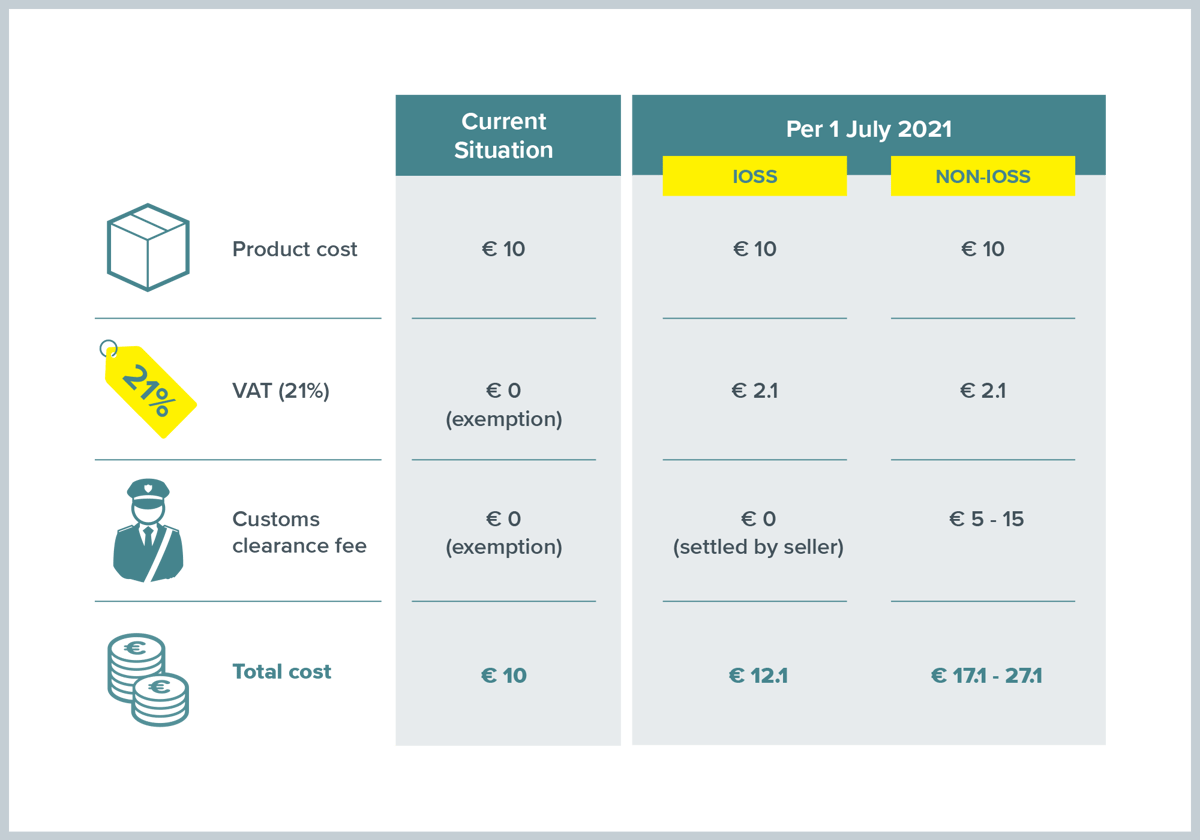

The new IOSS system is being introduced by the EU to simplify VAT for distance sellers in July 2021, alongside the removal of the EU’s low-value consignment relief of €22.

The introduction of IOSS is part of wider EU VAT reforms which are being implemented from 2021 onwards. Currently, both EU and non-EU e-tailers selling to EU consumers can import goods to the EU directly to the consumer without paying VAT if the consignment is valued at €22 or below. This is known as the low-value consignment VAT exemption, or “low value consignment relief”.

This VAT exemption, originally intended to save customs officials the hassle of checking large volumes of packages for minimal tax revenues, left EU-based online retailers at a disadvantage by requiring them to pay VAT for goods dispatched within the EU. The changes to VAT rules in 2021 will level the online playing field, as well as prevent fraudulent declarations attempting to evade VAT payments.

IOSS and new EU VAT rules explained

The Import One-Stop Shop (IOSS) provides an electronic portal created to centralise the declaration and payment of VAT for distance sales of imported goods (with a value not exceeding €150), making it easier, faster and simpler. The IOSS means the consumer/shopper is only charged once, at the time of purchase, so there are no surprise fees to pay when the goods are delivered. The VAT rate will be the one applicable in the EU Member State where the goods are to be delivered.

The new VAT rules will affect B2C consignments of standard goods (i.e. not subject to excise duties) imported into the EU and valued at €150 or less. It also means marketplaces will be responsible for charging and collecting VAT, acting as the deemed supplier for low-value consignments.

When do the changes come into effect?

From 01.04.2021

Sellers can register on the IOSS portal from 1 April 2021, but IOSS can only be used for goods sold from 1 July 2021.

From 01.07.2021

The EU is abolishing the low-value consignment relief for standard and reduced VAT goods to the EU from outside the EU.

![]()

How will IOSS affect my e-commerce business?

The simplest way to ensure compliance with the new rules is to register for IOSS.

The new VAT rules require an electronic interface (such as marketplaces or an e-commerce website) to clearly display the amount of VAT to be paid by the buyer in the EU prior to finalising the order, and ensure VAT is collected for goods being sent to any EU Member State.

All shipments will require a customs declaration, will be subject to VAT and must provide full and correct customs data. Remember, this will also include those shipments valued at equal to or less than €22, which are currently not subject to VAT.

Further requirements include (but are not limited to) submitting monthly electronic VAT returns via the IOSS portal and keeping records of sales facilitated by IOSS for 10 years.

What does it mean?

Seller and marketplaces (Electronic Interfaces) registered in the IOSS will pay the VAT collected on a sale to a consumer/shopper in an EU Member State. The VAT rate is the one applicable in the EU Member State where the goods are to be delivered.

From 1 April 2021, businesses can register on the IOSS portal of any EU member state that has published their registration process.

UK online sellers will need to appoint an EU-established IOSS intermediary or register via their eu entity to fulfil their VAT obligations under the IOSS scheme. the UK has not signed the VAT mutual assistance agreement with the EU (only Norway at the time of writing).

The IOSS registration is valid for all distance sales of imported goods to consumers in the EU.

The intermediary needs to be a taxable person established in the EU: it can be a law firm, authorised economic operator or European-based subsidiary of a non-EU based seller. The intermediary must be registered as an IOSS intermediarY.

FILL OUT OUR QUICK QUESTIONNAIRE AND WE WILL GET IN TOUCH WITH YOU TO PROVIDE RECOMMENDATIONS FOR IOSS INTERMEDIARIES.

Yes, Asendia is happy to recommend the right IOSS intermediary for your business; simply contact your Asendia account manager directly or fill out our quick questionnaire right now and we will get in touch with you to provide recommendations for IOSS intermediaries.

You can only start using the IOSS scheme from 1st July 2021. IOSS cannot be used for any transactions before 1st July 2021.

Asendia have no visibility of and are unable to influence the timeframe for the completion of your IOSS registration. We are under the impression all registrations will be completed by 1st July 2021, when IOSS comes into effect. Until that time, current processes will continue.

Once you are IOSS registered and have provided us with the necessary information, we don’t need to clear in the destination country.

If you do not have an IOSS number your items will be processed through our alternative network (for e-PAQ Select) and we can clear in destination with all tax charged back to you. For e-PAQ Standard and Plus this will work as it does today.

The new VAT rules apply to suppliers of services to EU consumers and sellers of goods to EU consumers (B2C), including marketplaces facilitating cross-border e-commerce. Postal operators as well as couriers will also need to comply with new customs regulations and declaration processes. Please be aware that OSS is for intra-EU distance sales; IOSS is for distance sales from non-EU origins to EU destinations.

The LVCR (low value consignment rate) doesn't apply (and never did apply) for B2B volumes

IOSS will only need to be considered across the following Asendia services: e-PAQ Standard, e-PAQ Plus, e-PAQ Select, e-PAQ Elite. All other services (e.g. Business Mail (prepared and part-prepared), Publications and Marketing Mail) are out of scope and will not change.

Please update your Asendia UK Account Manager with your unique number with us once you have it. Depending on how you are integrated with Asendia, two options are available: Asendia hardcode your IOSS number in our system and ensure that we pass this to Customs.

Alternatively, you reference your IOSS number in your manifest. If you are choosing to capture additional information in your manifest (other than your IOSS number), then please provide Asendia via your Account Manager, with a sample manifest as soon as possible, so we can sign off on its use and mitigate any delays.

The IOSS number is included in the data that we transmit on your behalf to the destination postal operator and they will use this to identify which parcels are subject to IOSS.

An electronic interface can include a website, portal, gateway, marketplace, app or any other system used to facilitate distance sales.

This term refers to the supplies of goods which are either dispatched or transported on behalf of the seller (from a third country or territory), to a consumer in EU Member States.

• If the goods are dispatched or transported from outside the EU at the time they are sold.

• If the goods are dispatched or transported in consignments with an intrinsic value of or up to €150.

• If the goods are not subject to excise duties (e.g. alcohol or tobacco products).

• If the electronic interface facilitates the direct sale of imported goods, or creates a contract between consumer and seller, where the end result of the sale of goods to that consumer.

The intrinsic value is the total value of goods in a consignment at the point of sale, excluding insurance, transport costs (unless they are included in the price and not indicated separately) and duties and taxes. If you would like to offer ‘shipping included in the price’, the shipping should be treated as 0 cost.

IOSS only impacts B2C goods, (please be advised excise goods are excluded from IOSS), if the items you send are not classed as B2C goods, then they will not be impacted. For example, our Service Destineo KDO is used for sending free gifts and samples and therefore will not be affected. All consignments equal or lower than €150 of an IOSS registered company must be declared under the IOSS scheme.

The EU considers the Marketplace liable for the VAT not the seller, so the Marketplace will be IOSS registered.

The online platform is liable for the collection of VAT on the supplies to final consumers / shoppers and for the remittance of this VAT to the tax administration. Marketplaces will be required to keep retailers' transactions in sufficient detail to enable tax authorities in the country of the customer to check that VAT has been correctly accounted for.

A marketplace will not be held liable for underpaid VAT on deemed retailer transactions where the retailer provided it with erroneous information that was required for the VAT calculation. You will need to provide the IOSS reference of the marketplace in your data /upfront so that we can clear the goods correctly

No. It is optional but when a company is IOSS registered it must comply with IOSS rules. IOSS will enable non-EU sellers to register in just one EU Member State to centralise their VAT declaration and payments for all EU-bound shipments.

We can manage Direct clearance across all destinations via our partner network. However, if you are not IOSS registered then there may be additional costs.

If you decide not to declare the VAT centrally, the Member State of consumption (the destination country in the EU) will become responsible for collecting VAT on the goods. If you are not registered for the IOSS scheme and are not using any customs prepaid solutions, any import tax and customs duties in the EU country of destination will be charged to the EU shopper upon delivery of the goods. This would considerably impact the shopping experience for your customers based in the EU.

For businesses outside of the EU, it is advisable to register under IOSS and appointing an EU-established intermediary to fulfil their VAT obligations under the IOSS scheme, unless the seller’s country has signed the VAT mutual assistance agreement with the EU (only Norway at the time of writing).

If a retailer is IOSS registered, the advantage is that clearance will be quicker as there will be no need to hold items for payment to be made. You will avoid potential bottlenecks at Customs and longer processing times. You will avoid potential delays to the final-mile delivery to the shopper, and avoid potential cost increases to the shopper on DDU orders and reduce abandoned packages.

If retailers choose not to become IOSS registered, they can still access DDP solutions for the destinations served by Asendia through a 'direct clearance' model (please see answer to question further below for list of countries within the direct clearance model).

Remember, high data quality reduces costs and transit times. Under declaration on Commercial Invoice or postal CN22/23 might lead to getting black-listed by the EU customs / tax authorities. Additional costs for examinations, penalties, etc

You can find more information on the EU Import one-stop Shop here: https://ec.europa.eu/taxation_customs/business/vat/ioss_en

Since 1st January 2021, the consignment data, content information and IOSS number are required for export and import purposes and must be entered electronically by the retailer to be sent to the country of destination in advance (electronic advance data – “EAD”). These regulations aim at implementing greater security (ICS2) as well as ensuring quicker customs processing, taking into account the growth of e-commerce worldwide. IOSS is transmitted within the EAD.

Many UK retailers have already ensured they are 'Brexit ready', for example by pre-advising electronic advance data for all shipments travelling by air, and so they are already operationally and data compliant for IOSS. But we advise that you still need to register for IOSS. It is important that the data quality for any postal traffic you may have is up to the same good standard.

Any additional information required to be provided by you (the retailer) in support of Customs Clearance, will be flagged within your Asendia shipping tools. These include: full sender and receiver details, parcel contents plus now the provision of your IOSS registration number in the data or upfront.

Please apply your IOSS number to field 44 (Country Registration Number) within the 49 field manifest. NB: the Asendia Shipping spec is due to be published w/c 7th June.

You will need to make changes to the API, please speak to your Account Manager. We are able to share details for the wnGobal API, and details for those accessing Asendia Shipping will be shared w/c 7th June

The IOSS number must not be on the label, commercial invoice or CN22/23

Asendia will hold the IOSS number into the system based on the information you provide, it doesn’t need to be on the label (thus mitigating against any potential GDPR or fraud issues).

There is no difference in the operational processes at origin and presentation to customs. Clearance is data driven, so any parcels which are not IOSS registered and need to be held for payment will be segregated by the receiving customs broker

There will be no changes necessary to how you present your traffic, there is no need to segregate items with a value under or above EUR 150, they can be presented mixed.

Our experienced brokers will determine dutiable/non-dutiable traffic based on the value of the goods using the exchange rate provided by the local customs authority.

A supplier or electronic interface or intermediary using the IOSS scheme should ensure the following in respect of VAT:

• Display a product's price and the VAT on its website;

• Collect the VAT amount when selling online;

• Check on the intrinsic value of the imported goods < €150;

• Mention the VAT on the invoice, distinguishing the different VAT rates

• Provide the customs declarant with the necessary information for customs clearance (including the IOSS VAT identification number)

• Filing a monthly VAT declaration before the end of month M+1

• Remit the VAT collected from the online sale before the end of month M+1

• Keep records of all eligible IOSS distance sales of imported goods for 10 years to cater for possible audits by EU tax authorities. The information to be retained is that provided for in Article 63c(2) of the VAT Implementing Regulation

When purchasing merchandise with an intrinsic value not exceeding €150 from an IOSS-registered company, shoppers will pay the EU VAT during the checkout process. This should be clearly displayed at all times so there are no hidden costs for consumers/shoppers. The IoR (Importer of Record) is still the consumer, however, VAT is effectively deferred at point of import. You will file tax returns via an intermediary who will ensure that the VAT you collected at checkout is passed to the relevant tax authority.

However, if the company is not IOSS-registered, if the order contains excise goods or if the value is above €150, it is likely that VAT and/or customs duty will be collected from the shoppers at reception. Import taxes collected at reception will also include the customs presentation fee of the destination country customs broker.

DAP (Incoterm) DDU: Delivered-at-place (DAP) is an international trade term used to describe a deal in which a seller agrees to pay all costs and suffer any potential losses of moving goods sold to a specific location. In delivered-at-place agreements, the buyer is responsible for paying import duties and any applicable taxes, including clearance and local taxes, once the shipment has arrived at the specified destination.

DDP (Incoterm): Delivered duty paid (DDP) is a delivery agreement whereby the seller assumes all responsibility of transporting the goods until they reach an agreed-upon destination. The risks to the seller are broad and include VAT charges, bribery, and storage costs if unexpected delays occur.

DTP (Trading term): Former e-DAP. Delivery Taxes paid corresponds to the process where the seller collects the duties and taxes, but the import of recorder is the buyer. Seller‘s Terms and Conditions should be clear about the ownership of goods transferring to the buyer before they enter the country. On a practical basis, DTP is DDP for the buyer but DAP for the Fiscal Representative. DTP is a trading term not an INCOTERM (Delivered at place, duty and Taxes Paid).

HS Codes: The Harmonized Commodity Description and Coding Systems (HS) is an international nomenclature for the classification of products. It allows participating countries to classify traded goods on a common basis for customs purposes. At the international level, the Harmonized System (HS) for classifying goods is a six-digit code system.

IOSS Tool - Single Reporting: A single report scheme covering sales of imported goods to EU consumers up to a value of €150 and for which a VAT exemption upon import will apply if the trader declares and pays the VAT at the time of the sale using this declarative system (called the Import One-Stop-Shop, or "IOSS").

LCC: The Landed Cost Calculator helps you determine an accurate estimate of the landed cost of your products by calculating the various import duties, VAT and excise taxes, and other government fees that will be added to your goods before they arrive at their destination.

IPC: International Post Corporation sets standards for upgrading quality and service performance and develops technology that helps members improve service for international letters, parcels and express.

PDDP: Postal Delivery Duties Paid (PDDP) is a service of the IPC which supports payment of taxes, duties and handling charges at the point of purchase by the e-buyer on the e-seller’s website and makes available the payable amount to the destination post for payment to customs.

ICS: The Import Control System is an electronic management system for security declarations used in postal and commercial processes for the import of goods into the European Union. All consignments from third countries into the EU must be declared in advance. The EU customs authorities will process a risk-based assessment based on this declaration.

EAD: EAD is the abbreviation for electronic advance data and refers to the electronic transmission of sender, recipient, content and consignment data. EAD is the abbreviation for electronic advance data and refers to the electronic transmission of sender, recipient, content and consignment data.

ITMATT: The Item Attribute is a UPU messaging standard used for provision of electronic customs information (i.e. an electronic CN 22/23) captured and transmitted by the origin designated operator to the destination designated operator at the time of mailing.

VAT: A value-added tax (VAT) is a consumption tax placed on a product whenever value is added at each stage of the supply chain, from production to the point of sale.

DUTY: Customs Duty is a tariff or tax imposed on goods when transported across international borders. The purpose of Customs Duty is to protect each country's economy, residents, jobs, environment, etc., by controlling the flow of goods, especially restrictive and prohibited goods, into and out of the country.

IOR: Importer of Record: In most cases, the Importer of Record (IoR) is the person or entity who actually has ownership of the imported goods at the time of import. For e-commerce shipments the consumer is usually the Importer of Record (with the broker acting on their behalf for the purposes of declaring the items to the local customs authority); however there are other shipping methods which allow for the sender to be the Importer of Record.

.png?width=500&name=Asendia-Customs-3d%20(1).png)